Executive Context

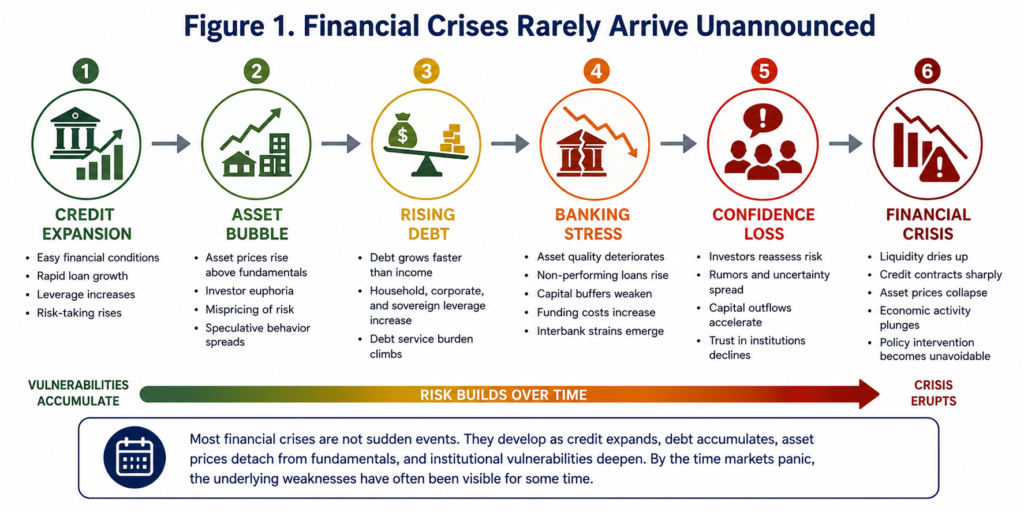

Financial crises are often described as sudden shocks. In reality, most of them build over time.

Before a banking system weakens, before a currency comes under pressure, before sovereign debt becomes difficult to service, and before inflation erodes confidence, the warning signs usually appear in the data. The problem is not always that governments, investors, or regulators lack information. More often, the problem is that available information is fragmented, misread, delayed, or ignored.

Financial crises follow patterns. Credit expands faster than income. Asset prices rise beyond fundamentals. Public debt grows faster than revenue. Banks report strong profits while asset quality deteriorates beneath the surface. Foreign reserves decline while exchange-rate pressures are managed through temporary interventions. Investors continue pricing risk as though favorable conditions will continue indefinitely.

Visual direction: A left-to-right timeline showing: Credit Expansion → Asset Bubble → Rising Debt → Banking Stress → Confidence Loss → Financial Crisis.

By the time panic becomes visible, the most effective policy options may already have narrowed.

Table 1. Typical Crisis Progression

| Stage | Primary Characteristic | Key Risk |

|---|---|---|

| Credit Expansion | Rapid lending growth | Excess leverage |

| Asset Bubble | Prices exceed fundamentals | Mispricing of risk |

| Rising Debt | Debt grows faster than income | Repayment pressure |

| Banking Stress | Asset quality deteriorates | Financial instability |

| Confidence Loss | Investors reassess risk | Capital flight |

| Financial Crisis | System-wide disruption | Recession and intervention |

This is why crisis prediction should not be treated as an academic exercise. It is a practical governance, investment, and institutional-resilience tool. No model can predict every crisis with perfect accuracy, but disciplined early warning systems can identify rising vulnerability early enough for governments, investors, and development partners to act before stress becomes systemic.

ABT Investment & Consulting LLC views financial crisis prediction as part of a broader policy and investment-risk architecture. The objective is not only to identify economic weakness. The objective is to understand how financial pressure moves across banks, governments, markets, households, and institutions.

The Policy Challenge

Financial crises become more damaging when decision-makers confuse temporary stress with structural weakness.

A country may treat a falling currency as a short-term market problem when it actually reflects deeper reserve, fiscal, and confidence pressures. A regulator may treat a bank’s funding shortage as a liquidity issue when the institution’s balance sheet is already impaired. A government may describe debt concerns as manageable because debt-to-GDP appears moderate, even while debt service consumes a dangerous share of public revenue.

These misreadings matter because crisis response depends on correct diagnosis.

A liquidity problem requires one set of tools. A solvency problem requires another. A currency crisis requires different interventions from a banking crisis. A sovereign debt crisis cannot be solved with communication alone if the fiscal structure is no longer credible.

The policy challenge, therefore, is not simply to collect more data. It is to build systems that interpret data correctly, distinguish between surface symptoms and underlying vulnerabilities, and connect warning signals to timely action.

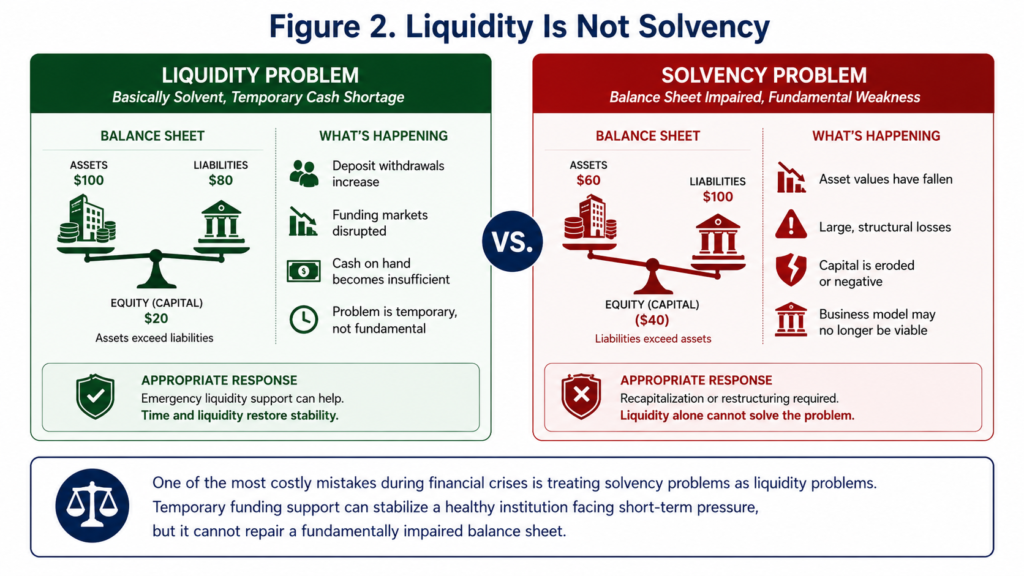

Why Liquidity and Solvency Must Be Distinguished

One of the most important distinctions in financial crisis management is the difference between liquidity and solvency.

A liquidity problem occurs when an institution has fundamentally sound assets but does not have enough immediate cash or marketable assets to meet short-term obligations. This can happen during deposit withdrawals, market freezes, or sudden funding disruptions. In such cases, temporary central bank support, emergency lending facilities, or market-stabilization tools may help contain the stress.

A solvency problem is deeper. It occurs when the value of an institution’s liabilities exceeds the value of its assets. In that situation, the institution is not merely short of cash. It is financially impaired. More liquidity may delay failure, but it cannot restore balance-sheet health unless the underlying losses are addressed.

Visual direction: A split-screen graphic. On the left: Liquidity Problem — good assets, temporary cash shortage, deposit withdrawals, funding disruption, emergency lending can help. On the right: Solvency Problem — assets worth less than liabilities, capital erosion, structural losses, recapitalization or restructuring required.

This distinction is critical because treating a solvency crisis as a liquidity crisis can prolong instability. It can also transfer losses to taxpayers, weaken public confidence, and allow weak institutions to continue operating without real repair.

Table 2. Liquidity vs. Solvency

| Characteristic | Liquidity Problem | Solvency Problem |

|---|---|---|

| Assets exceed liabilities | Yes | No |

| Cash available immediately | Insufficient | Often insufficient |

| Temporary central bank support may help | Yes | Limited effect |

| Requires recapitalization | Usually no | Usually yes |

| Can become systemic if ignored | Yes | Yes |

| Represents structural weakness | No | Yes |

Many crises begin with liquidity pressure but become solvency crises when asset values fall, loan losses rise, and confidence disappears. Effective early warning systems must therefore monitor both short-term funding stress and deeper balance-sheet weakness.

Liquidity indicators include deposit outflows, funding concentration, liquidity coverage, loan-to-deposit ratios, short-term refinancing needs, and reliance on emergency facilities.

Solvency indicators include capital adequacy, leverage, asset quality, non-performing loans, loss provisions, debt-service capacity, and exposure to declining asset values.

The distinction is technical, but its consequences are practical. A system that cannot separate liquidity stress from insolvency risk will respond late, respond wrongly, or both.

How Crises Build

Financial crises rarely begin with visible panic. They usually begin during periods of confidence.

Credit becomes easier to obtain. Banks expand lending. Governments borrow with little market resistance. Investors search for yield. Asset prices rise. Policymakers assume that growth, capital inflows, or commodity revenues will continue.

This is why early warning systems must look beneath favorable headline numbers.

Strong GDP growth may conceal excessive borrowing. Rising bank profits may conceal weakening loan quality. Stable exchange rates may conceal heavy reserve intervention. Large infrastructure spending may conceal weak fiscal returns. Low borrowing costs may conceal future rollover risk.

The danger is not only economic weakness. The danger is misplaced confidence.

When confidence finally turns, adjustment can be abrupt. Depositors withdraw funds. Investors demand higher yields. Exchange rates fall. Central banks raise interest rates. Borrowers struggle to repay. Governments face higher debt-service costs. What appeared manageable can quickly become systemic.

Visual direction: An iceberg graphic. Above the water: GDP Growth, Rising Markets, Strong Earnings, Stable Exchange Rate. Below the water: Hidden Loan Losses, Excessive Leverage, Reserve Depletion, Fiscal Weakness, Political Risk.

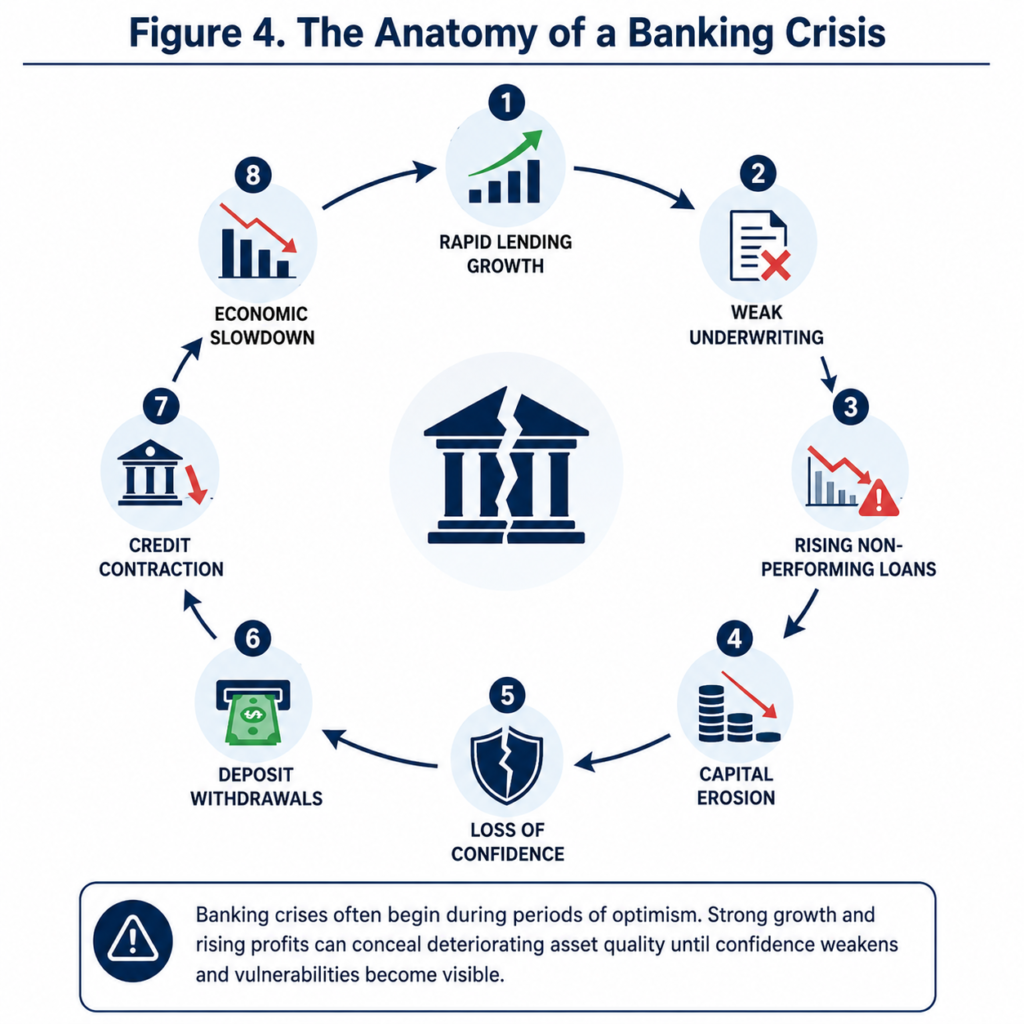

Banking Crises

Banking crises are particularly dangerous because banks sit at the center of economic life. They connect households, businesses, governments, and financial markets.

A banking crisis may begin quietly through poor lending decisions, weak supervision, rapid credit growth, high exposure to one sector, or rising non-performing loans. During good times, these problems may be hidden by strong earnings or asset-price appreciation.

The warning signs become clearer when loan losses rise, capital buffers shrink, liquidity tightens, depositors lose confidence, and banks reduce credit to the real economy.

The key question for policymakers is not whether a bank is currently open for business. The question is whether its balance sheet can withstand stress.

A banking system may appear stable until market confidence shifts. Once confidence weakens, even institutions with temporary liquidity pressures can face severe funding stress. If underlying asset quality is also poor, liquidity support alone may not be enough.

Currency Crises

Currency crises occur when confidence in a country’s exchange-rate position weakens.

This may result from falling reserves, current-account pressures, capital flight, political uncertainty, high inflation, or loss of confidence in monetary policy. In some cases, authorities defend the currency through reserve sales or administrative controls. These tools may buy time, but they do not solve the underlying problem if external imbalances persist.

Currency pressure is especially damaging because it moves quickly into other parts of the economy. Depreciation can raise import costs, increase inflation, worsen foreign-currency debt burdens, and weaken investor confidence.

A stable exchange rate does not always mean the system is healthy. If stability depends on unsustainable intervention, delayed payments, or restricted access to foreign exchange, hidden pressure may be accumulating.

Sovereign Debt Crises

Sovereign debt crises occur when governments lose the ability to borrow or repay on sustainable terms.

Debt-to-GDP is often used as the headline indicator, but it is not enough. A country with moderate debt may still face stress if public revenue is weak, debt service is high, maturities are short, or a large share of debt is denominated in foreign currency.

Markets are often less concerned with the size of debt in isolation than with the government’s capacity to service it.

Debt-service-to-revenue, interest-payments-to-revenue, rollover needs, currency composition, and investor demand often provide a clearer picture of fiscal vulnerability than debt stock alone.

A sovereign debt crisis is also a credibility crisis. Once investors believe that the fiscal path is no longer sustainable, borrowing costs rise. Higher borrowing costs then worsen the very problem that markets fear.

Inflation Crises

Inflation crises weaken economies from the household level upward.

When prices rise persistently, wages lose value, savings lose purchasing power, businesses struggle to plan, and central banks face pressure to raise interest rates. Higher interest rates may be necessary to restore credibility, but they also raise borrowing costs for households, firms, and governments.

Inflation becomes especially dangerous when it is linked to currency weakness, fiscal deficits, supply shortages, or monetary financing of government spending.

Food inflation deserves special attention because it affects social stability directly. When basic consumption becomes unaffordable, financial stress can quickly become political stress.

Inflation is not only a price problem. It is a confidence problem.

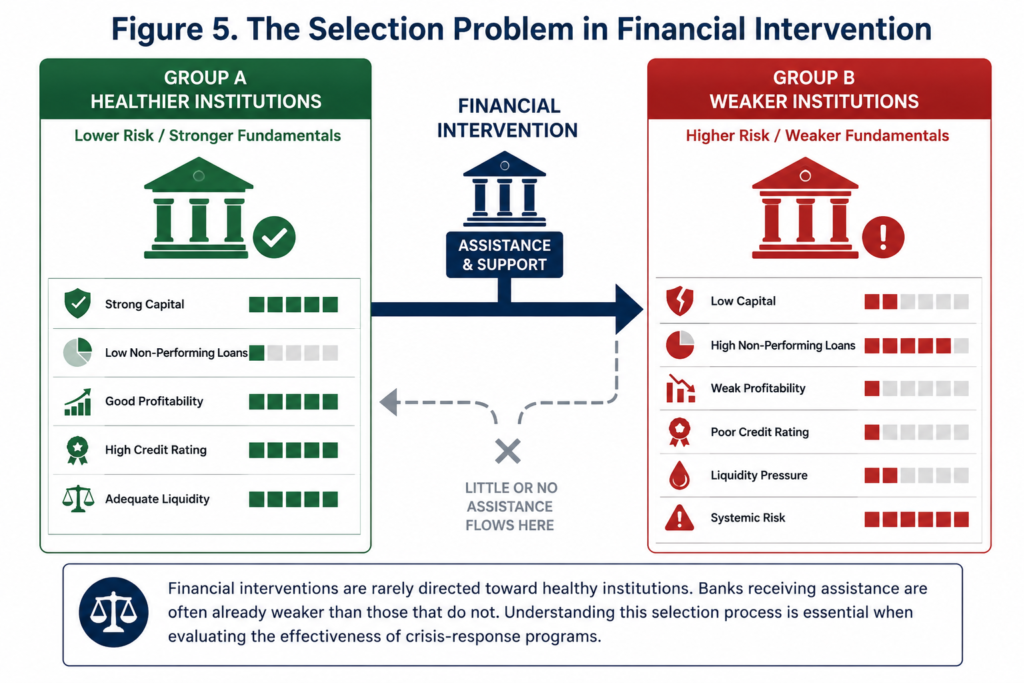

The Selection Problem in Crisis Prediction

A less visible challenge in crisis prediction is the selection problem.

During financial stress, interventions are rarely random. Regulators, governments, and central banks usually direct assistance toward institutions already showing signs of weakness. Banks with high non-performing loans, capital shortfalls, poor supervisory ratings, or systemic importance are more likely to receive support.

This creates a problem for analysis.

If assisted banks later perform poorly, observers may conclude that the intervention failed. That may be true in some cases. But it may also be that these banks were already weaker than those that did not receive support.

The same logic applies to countries, firms, and financial markets. Those receiving emergency support are often already on a weaker path. Their post-intervention outcomes reflect both the effect of assistance and the vulnerabilities that made assistance necessary.

This matters for early warning systems because crisis prediction is not only about observing outcomes. It is also about understanding why certain institutions became vulnerable in the first place.

A serious risk framework must therefore examine both selected and non-selected cases. It must compare distressed institutions with those that remained resilient. It must ask whether observed stability is genuine or merely the result of temporary intervention.

This is where advanced tools such as selection models, stress testing, probability models, and scenario analysis become useful. They help separate visible intervention effects from underlying fragility.

For policymakers, the lesson is clear. Do not judge crisis programs only by what happens after assistance is provided. Examine the conditions that made assistance necessary.

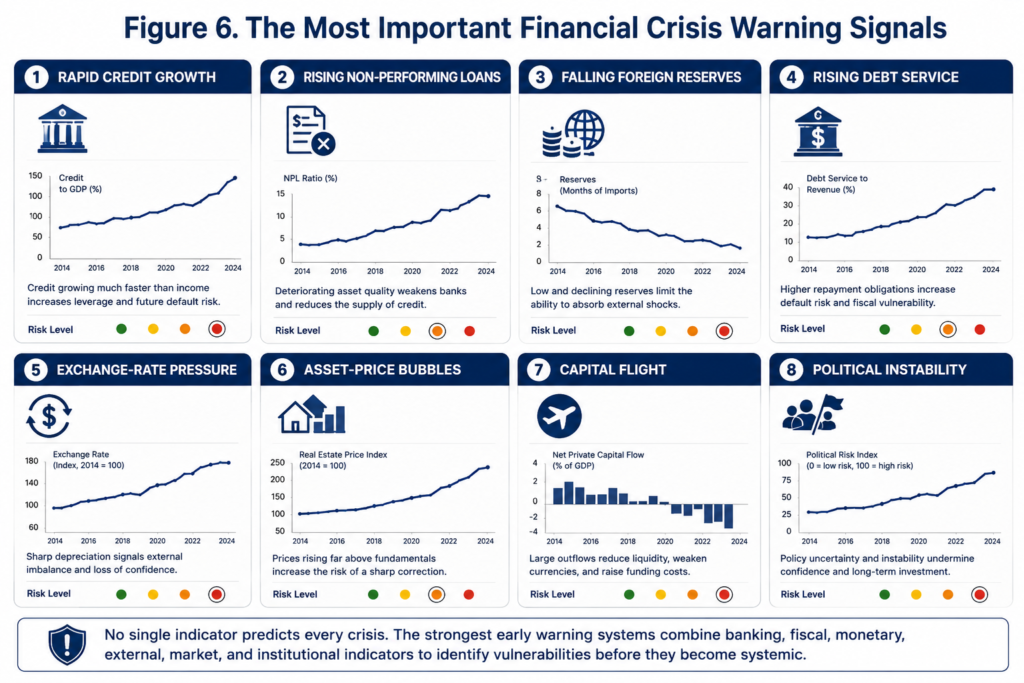

Core Early Warning Signals

A credible early warning system must combine several categories of risk.

Credit growth is one of the strongest signals. When lending expands faster than income or productivity, repayment risk may be building. This is especially dangerous when credit flows into real estate, consumption, foreign-currency borrowing, or politically connected sectors.

Asset prices also matter. Rapid increases in real estate, equity, or commodity-linked assets may reflect optimism, but they may also indicate leverage-driven speculation. The danger comes when prices are supported more by borrowing than by earnings.

Banking indicators are essential. Rising non-performing loans, declining capital adequacy, weak liquidity, loan concentration, and falling profitability can signal deeper financial-sector stress.

Foreign reserves provide another warning channel. A country with declining reserves, high import needs, short-term external obligations, and capital outflows may face growing currency vulnerability.

Exchange-rate pressure is often a visible symptom of deeper weakness. Sharp depreciation, widening market premiums, foreign exchange shortages, and rising dollarization all point to confidence risk.

Debt-service pressure is central to fiscal vulnerability. Governments do not default because debt exists. They default, restructure, or seek emergency support when repayment obligations exceed fiscal capacity.

Market signals also matter. Rising sovereign yields, widening credit spreads, rating downgrades, weak auction demand, and capital outflows often reveal investor concern before official statements acknowledge stress.

Political and institutional signals must not be ignored. Policy reversals, weak central bank independence, corruption concerns, regulatory unpredictability, election-related spending, and poor data credibility can all turn financial stress into full crisis.

Building an Effective Early Warning System

An early warning system should begin with a clear definition of crisis risk.

The relevant event may be a banking failure, debt restructuring, emergency bailout, currency collapse, reserve crisis, inflation surge, or systemic liquidity freeze. Without a clear definition, the model cannot determine what it is trying to detect.

The next step is to build an integrated dashboard. This dashboard should bring together monetary, fiscal, banking, external, market, and institutional indicators. The point is not to create a large spreadsheet. The point is to show how pressure moves across the system.

For example, inflation may force interest rates upward. Higher rates may weaken borrowers. Weaker borrowers may increase loan losses. Rising loan losses may reduce bank lending. Lower credit may slow growth. Slower growth may reduce revenue. Lower revenue may worsen debt-service pressure.

A good dashboard reveals these linkages early.

Thresholds should then be established. These thresholds must be country-specific and institution-specific. A reserve level that is adequate in one economy may be weak in another. A debt ratio that is manageable in a high-revenue country may be dangerous in a low-revenue country. A credit boom may support productive investment in one setting and speculative excess in another.

Statistical and analytical models can strengthen the process. Logit and probit models can estimate the probability of crisis. Survival models can examine time to distress. Stress tests can measure resilience under adverse scenarios. Machine learning can identify non-linear patterns across large datasets.

These tools should support judgment, not replace it.

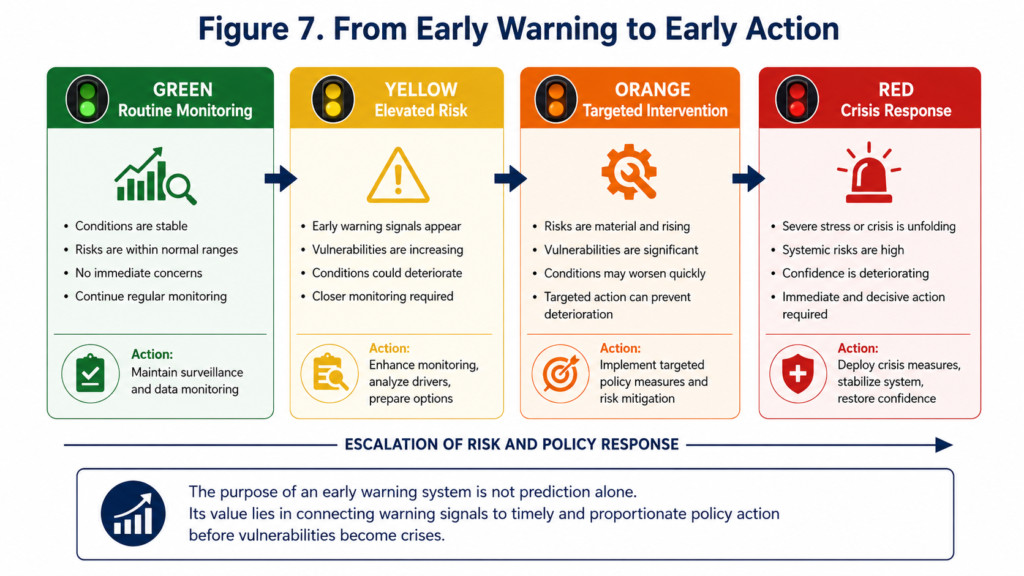

The most important feature of an early warning system is not technical sophistication. It is whether warning signals are connected to decisions.

A yellow signal should trigger closer monitoring. An orange signal should trigger targeted intervention. A red signal should trigger urgent stabilization planning. Without this link, early warning becomes early observation rather than early action.

Strategic Recommendations

1. Treat Crisis Prediction as Governance Infrastructure

Governments and institutions should not treat crisis prediction as a temporary research project. It should be part of national economic management, financial supervision, investor-risk assessment, and development planning.

2. Distinguish Liquidity Support from Solvency Repair

Emergency liquidity can stabilize markets, but it cannot solve insolvency. Policymakers must assess whether stress reflects temporary funding pressure or deeper balance-sheet weakness.

3. Monitor Debt Service, Not Debt Stock Alone

Debt-to-GDP remains useful, but it is insufficient. Debt-service-to-revenue, interest costs, rollover risk, currency composition, and maturity structure provide a more practical view of fiscal stress.

4. Watch Credit Booms Before Losses Appear

Credit booms often look healthy before they become dangerous. Regulators should monitor whether lending growth is tied to productive investment or speculative activity.

5. Strengthen Banking Supervision Before Panic

Supervision must be forward-looking. Waiting for bank failures before acting defeats the purpose of financial stability policy.

6. Include Political Risk in Financial Risk Models

Financial systems depend on confidence. Confidence depends on institutions. Policy inconsistency, weak governance, and poor data credibility should be treated as financial stability risks.

7. Account for Selection Bias in Intervention Analysis

Institutions that receive support are often already weaker than those that do not. Evaluating crisis programs without accounting for this difference can produce misleading conclusions.

8. Link Warning Signals to Clear Policy Action

Every major risk indicator should be tied to a response plan, responsible institution, reporting timeline, and escalation process.

Implications for Governments and Investors

For governments, early warning systems reduce the cost of crisis response. They help preserve fiscal space, protect households, and maintain policy credibility.

For investors, they improve country-risk assessment, portfolio allocation, and exposure management.

For central banks and regulators, they strengthen supervision, liquidity planning, and systemic-risk monitoring.

For development institutions, they support better technical assistance, debt sustainability analysis, emergency financing, and institutional reform design.

The central point is simple. Crisis prevention is less costly than crisis management.

The ABT Advisory Perspective

ABT Investment & Consulting LLC approaches financial crisis prediction as a policy, governance, and investment-risk discipline.

Our advisory model integrates macroeconomic risk analysis, financial-sector vulnerability assessment, debt sustainability monitoring, banking-sector diagnostics, early warning dashboards, scenario modeling, and policy response design.

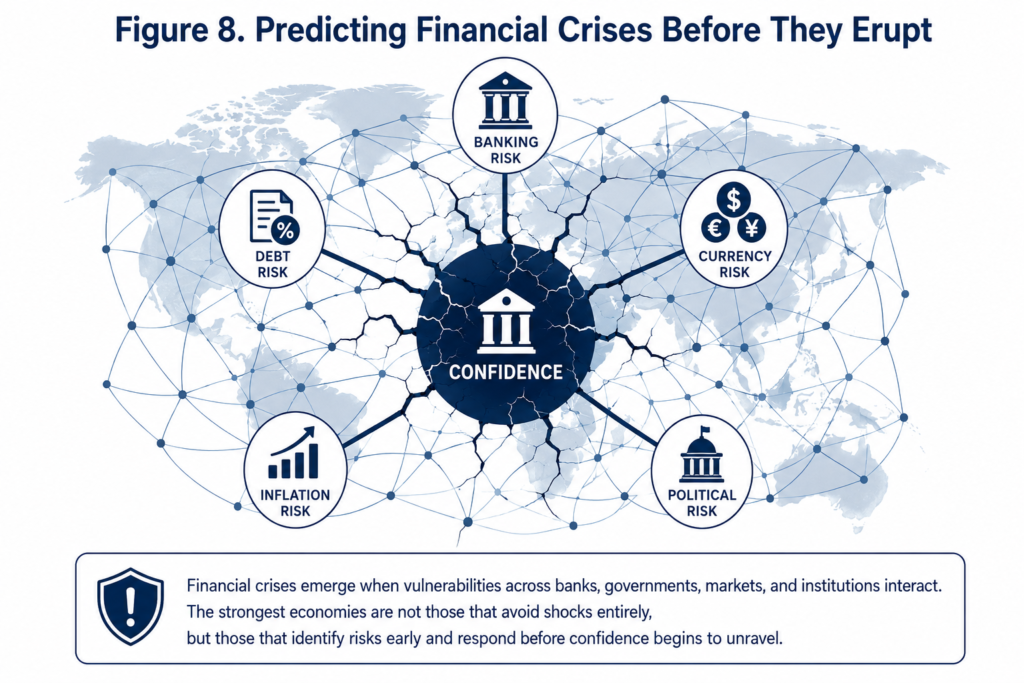

Financial crises are rarely caused by one variable. They emerge when weaknesses interact across balance sheets, public finances, markets, households, and institutions.

ABT supports governments, investors, and development partners in identifying these vulnerabilities early and translating risk signals into practical decisions.

The strongest institutions are not those that assume stability will continue. They are those that prepare for stress before confidence begins to break.

Conclusion

Financial crises do not begin when markets panic. They begin earlier, in excessive credit growth, weak supervision, rising debt burdens, falling reserves, currency pressure, inflation, and institutional complacency.

The historical record shows that crises are rarely completely invisible. What is often missing is the willingness to act on early evidence.

Effective crisis prediction therefore requires more than data. It requires credible institutions, honest reporting, disciplined analysis, and decision-makers prepared to respond before conditions deteriorate.

For governments, investors, and development institutions, the priority is clear.

Build stronger early warning systems. Separate liquidity problems from solvency problems. Monitor risk across sectors. Treat confidence as a financial asset. Act before stress becomes crisis.

The cost of preparation is far lower than the cost of collapse.

0 Comments